Healthcare Cost Drivers Secretly Killing Your Success

There has been no lack of words describing the pitfalls of the American healthcare system. You’ve likely heard all of them.

Recently, my daughter went to urgent care with a suspected case of meningitis. Fortunately, she was ok and learned she was suffering from a "common virus."

However, after doing the right thing by going to urgent care first, she was immediately redirected to the emergency room. Still waiting for the last of the bills to arrive, she has already incurred charges in excess of $10,000.

Perhaps it was just bad luck. Then again, maybe it was all by design.

This is a story that happens to the well-intended far too often.

It has me reflecting on all the ways we encounter expense drivers that simply remain unseen. Until we bring light into that darkness, nothing will change.

Today, we address five healthcare cost drivers receiving too little attention.

In no particular order, these are the special few that we all need to spend a little more time thinking about and considering how we can mitigate or temper their negative influences.

Insurance Companies

Healthcare Aggregation

The Pharmaceutical Quagmire

Brokers and Insurance Agencies

Human Nature

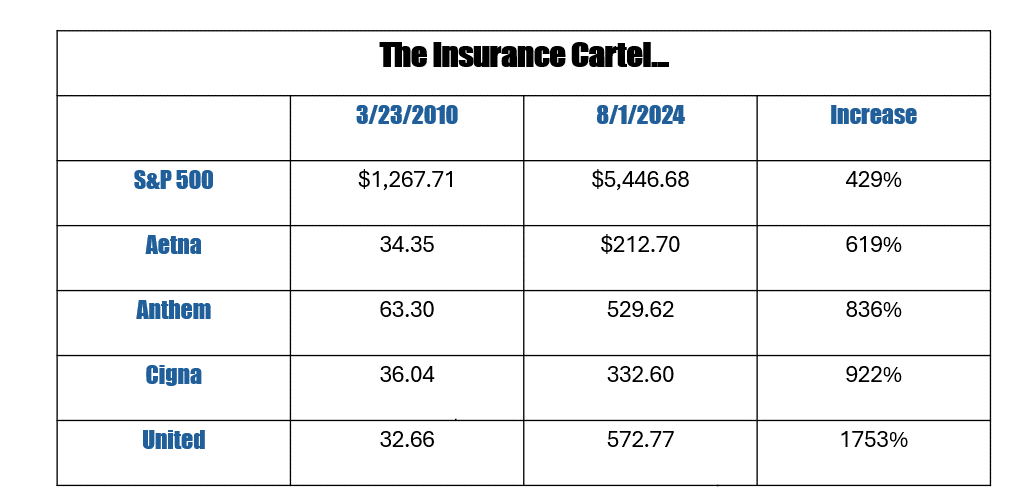

Insurance Companies

Innovation hasn’t died, but it has largely been thwarted by the ever-present need to generate profits.

This seems to be especially true when we take a look at America's largest insurance companies.

The Affordable Care Act attempted to temper the profitability of insurance companies by introducing the Medical Loss Ratio (MLR).

This capped how much an insurance company could capture for operational expenses and required a pre-determined ratio to be dedicated to claims payments. (Insurance companies can retain 20% for small groups and 15% for large groups.)

However, the MLR effectively codified insurance companies' profitability. As a result, service, innovation, and cost containment have arguably suffered.

When you are guaranteed revenue on 15% of the premium, how do you grow that revenue?

You have to increase premiums.

MLR has created a fundamental conflict for insurance companies. While they have the resources and ability to create a different cost trajectory for their insureds, doing so is not in the interest of their shareholders.

Most employers could benefit from a pivot towards self-insuring and unbundling, giving you control, financial transparency, and access to data at a level that does not exist under these traditional arrangements.

Healthcare Aggregation

When it comes to dysfunction, one of the under-cited sources of inflation has to do with the number of aggregators and consolidators constantly at play in the healthcare delivery continuum. Whether it’s insurance companies buying pharmacy benefit managers (or other insurance companies), health systems buying medical practices, insurance companies buying physician practices, the proliferation of new hospitals, or health systems and third-party companies popping up stand-alone emergency rooms, there has been a massive expansion of investment dollars into a smaller pool of players — all created to increase market share and increase profits.

In his book Cheated, Alan Wiederhold shares that private entities' annual value of acquired healthcare servicesincreased from $42 billion in 2010 to approximately $120 billion in 2019.

He shares a quote attributed to the Private Equity Healthcare report: "Private equity funds, by design, are focused on short-term revenue generation and consolidation and not on the care and long-term wellbeing of patients. This, in turn, leads to pressure to prioritize revenue over the quality of care, and overburden health care companies.”

The 30,000-foot view suggests that aggregation reduces competition, increases market share, increases profitability, increases internal referral opportunities, and gives health systems more significant clout to negotiate richer contracts while also focusing on quantity over quality.

None of this betters the experience or cost containment.

I suspect this may have been the root cause of my daughter's being redirected to the emergency room. The urgent care she visited was owned by the same company that owned the hospital.

It makes you wonder if the urgent care environment has been intentionally limited in order to create greater revenue for health system.

The Pharmaceutical Quagmire

The number of ways that the pharma industry impacts our healthcare pricing is too long and too complex to capture here fully. And frankly, I’m no expert in this area. However, some primary culprits are the FDA, the manufacturers, and the pharmacy benefit managers.

One of the most helpful resources I recommend to everyone is the book The Price We Pay by Dr. Marty Makary. In the chapterPharmacy Hieroglyphics, he details the destructive financial impacts of pharmacy benefit managers onprescription pricing.

Makary shared the following anecdote in his book:

Cookie Benefit Manager

“Think about how this PBM game might look if it happens to another important commodity: Girl Scout cookies. Let’s say a dad approaches the CEO of a small company and offers to provide discounted Girl Scout cookies services to the company’s 100 employees. The busy CEO has no idea how much the different boxes of Girl Scout cookies normally cost (who does?) but he likes the simplicity of getting all his cookies from one guy. And he’s intrigued by the promise of bulk discounts the dad claims he can pass along to the company. The CEO agrees to make the dad the exclusive Girl Scout manager for his employees.

“A week later, the dad arranges for a few young Girl Scouts to set up a stand at the company office. One employee walks up and asks for a box of Thin Mints — everybody’s favorite. The girl says it will cost him only $2. He pays the $2 “copay” for his box and gobbles them up. The girls go on to a sell a hundred boxes. The CEO is glad to see his employees enjoying the cookies.

“A week later, the dad arranges for a few young Girl Scouts to set up a stand at the company office. One employee walks up and asks for a box of Thin Mints — everybody’s favorite. The girl says it will cost him only $2. He pays the $2 “copay” for his box and gobbles them up. The girls go on to a sell a hundred boxes. The CEO is glad to see his employees enjoying the cookies.

”A month later, the dad bills the company’s CEO a whoping $50 per box, and subtracts the “20% discount” bringing the bill to roughly $40 per box. The busy CEO can’t decipher the bill but pays it anyway, comforted by the 20% discount reflected on the bill.

“The dad then gives the Girl Scouts $1 for each box that they sold, so the girls collect a total of $3 per box (the $2 copay from the employee + $1 from the cookie manager). Their wholesol cost is $2.50, so the girls make 50 cents per box. The dad makes $39 per box, or $3,900 for the day for “managing the employee cookie benefit.”

Dr. Mary Makary, The Price We Pay

In this analogy, the dad is the PBM and the girl scouts are the pharmacies. Today, approximately 80% of Americans get their medications through a PBM. The system is a mess, and we can do better.

Brokers and Insurance Agencies

Both authors referenced above, Wiederhold and Makary, blame contingency or bonus programs provided by insurance companies as the driver of the status quo.

With massive consolidation in the industry, there are fewer payors available for brokers to represent. In some markets, there may be as few as two or three insurance companies available to offer to employer clients.

Every one of those insurance companies incentivizes brokers with both new and renewal bonuses to assure they are maximizing their market position, and those bonuses can add up.

They are not wrong to suggest this may be a driver.

But they are not entirely right, either.

Brokers and insurance agencies are not on this listbecause of the financial mechanics of compensation.

It’s because they are lazy. Complacency is the real contributor.

The reality is that more innovation has been introduced to the marketplace in the last seven to nine years than in the twenty years prior to that. Niche vendors have exploded, and point solutions abound. Each offers a new strategy or methodology to cost containment. Data analytic platforms have proliferated. Third-party Administrators have transformed from check-payers to true advocates. Healthcare navigational resources have become abundant. More resources are available today to help employers manage claims expenses than ever before.

The innovative stuff takes work, is hard to learn, and can be burdensome to quote. Vendor relationship managers change often, making it difficult to stay in touch. It’s also difficult to know which vendors actually do cool stuff instead of just saying cool stuff. It just takes a lot of work.

Instead of doing that work, many brokers take the safe route. They pick one or two insurance companies, put nearly all of their clients with them, and tell their clients that their large blocks of business give them the clout to negotiate better deals.

Human Nature

Maybe it’s you, the individual who’s reading this. Maybe it’s the collective you. Maybe it’s the corporate you.

Maybe it’s all of us.

But we are our own worst enemies. It’s human nature.

A quick Google search of “lifestyle impact on health costs” brought up hundreds of articles. Here are a few of the best headlines:

Changing lifestyle choices could cut $730B in annual health care spending

Unhealthy choices cost company health care plans billions of dollars

Modifiable Health Risks Linked to more than $730 Billion in US Health Care Costs

Should we go on?

If we all made a more concerted effort to take care of ourselves, we wouldn’t need to be so egregiously offended by the behaviors of insurance companies, aggregators, pharmaceuticals, and brokers.

Ultimately, you are the problem. I am the problem. We are the problem. The articles above indicated that lifestyle modification could impact up to $730 Billion in annual healthcare spending. Until we get serious about doing everything in our power not to be the problem, I’m not sure any of the rest of it matters.

Not only should we do a better job taking care of our health, but we must turn every stone. You are obligated to yourself, your company, your employees, your customers, and your community to be a part of the solution.

Rest assured, there are solutions. For every bad apple, there are dozens of good apples. It just takes some work to pick through the barrel.

Please let me know if I can help do the picking.